When a Billion Dollar Outcome Isn’t Enough

3/31/24 Benchmarks for Operators

My goal is to create the best valuation and performance benchmarks specifically for tech operators. If you are in Finance, Strategy, or Operations, this will help you translate what the outside world values to your target operating model.

When a Billion Dollar Outcome Isn’t Enough

Venture fund returns typically follow a power law (e.g., 80% of the returns are generated by 20% of the investments).

As a rule of thumb, investors will often want to see a scenario where any given company could theoretically return the fund 1x.

So if you are talking to an investor managing a $500M fund, the investor would be looking for a $500M return potential. The simple math then would be in order to generate $500M returns, at 20% ownership the company needs to be valued at $2.5B at exit. Assuming we are looking at a software company we could very simplistically assume a 10x exit revenue multiple (generous!) which would imply the company needs to reach $250M in revenue at exit.

I was talking to a friend who’s a Series B / C / D investor. He said:

“I’ve definitely struggled with having to tell founders that a $1B exit may not be big enough. By any standard, building a company to a $1B exit is an incredible accomplishment, yet for a large fund the absolute return dollars are often too small to move the needle.”

As an operator, you should absolutely do the back of the envelope math on what a “good” outcome would look like for your investors. That’s in essence what you are signing up for when you take the cash.

And there’s certainly some sticker shock when you realize that a lifechanging, generational wealth creating event might actually be a “mehhh” outcome for your backers. But don’t hate the player, hate the game. So keep an eye on that pref stack!

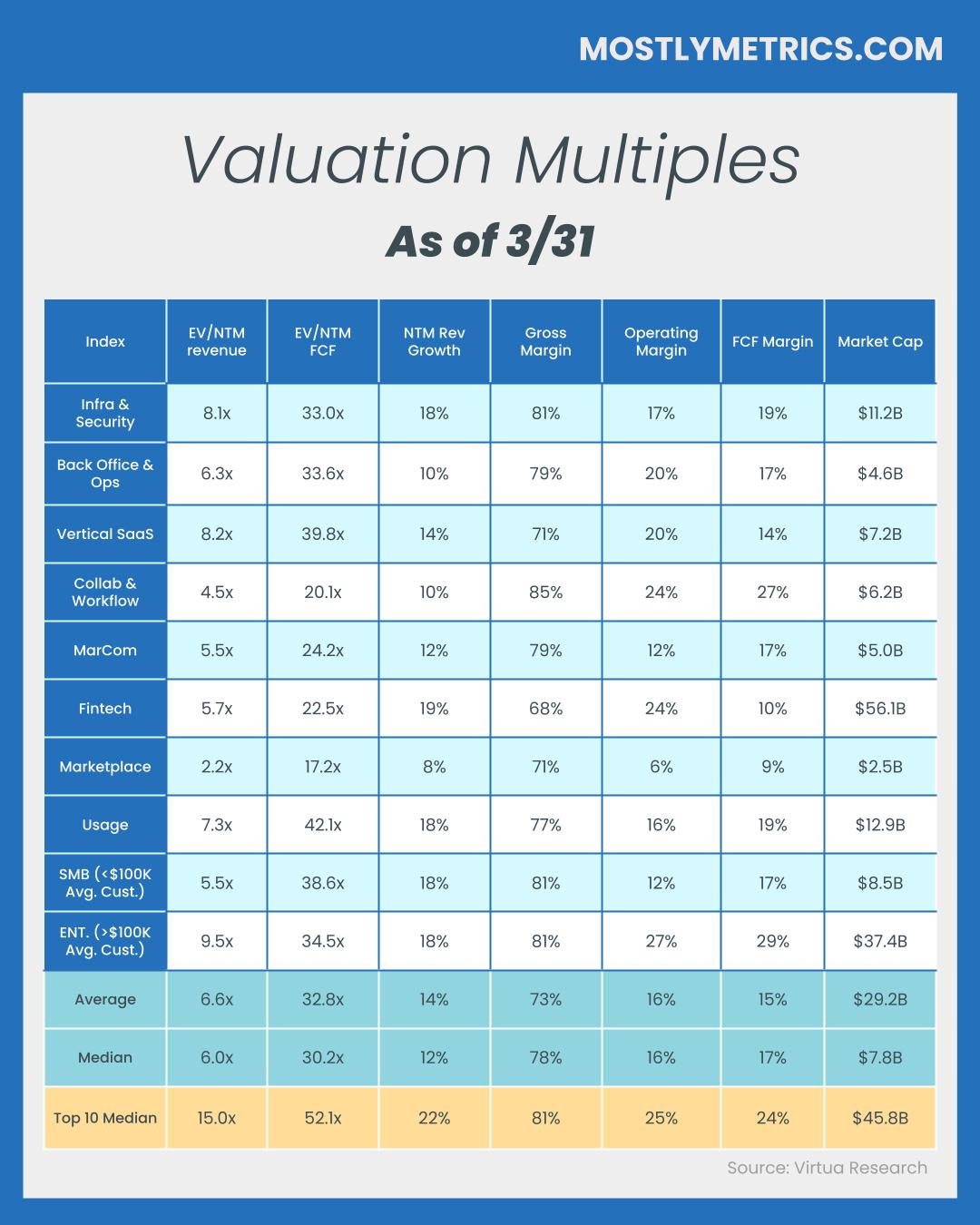

Figures for each index are measured at the Median

Average, Median, and Top 10 Median are measured across the entire data set, where n = 151

All margins are non-gaap

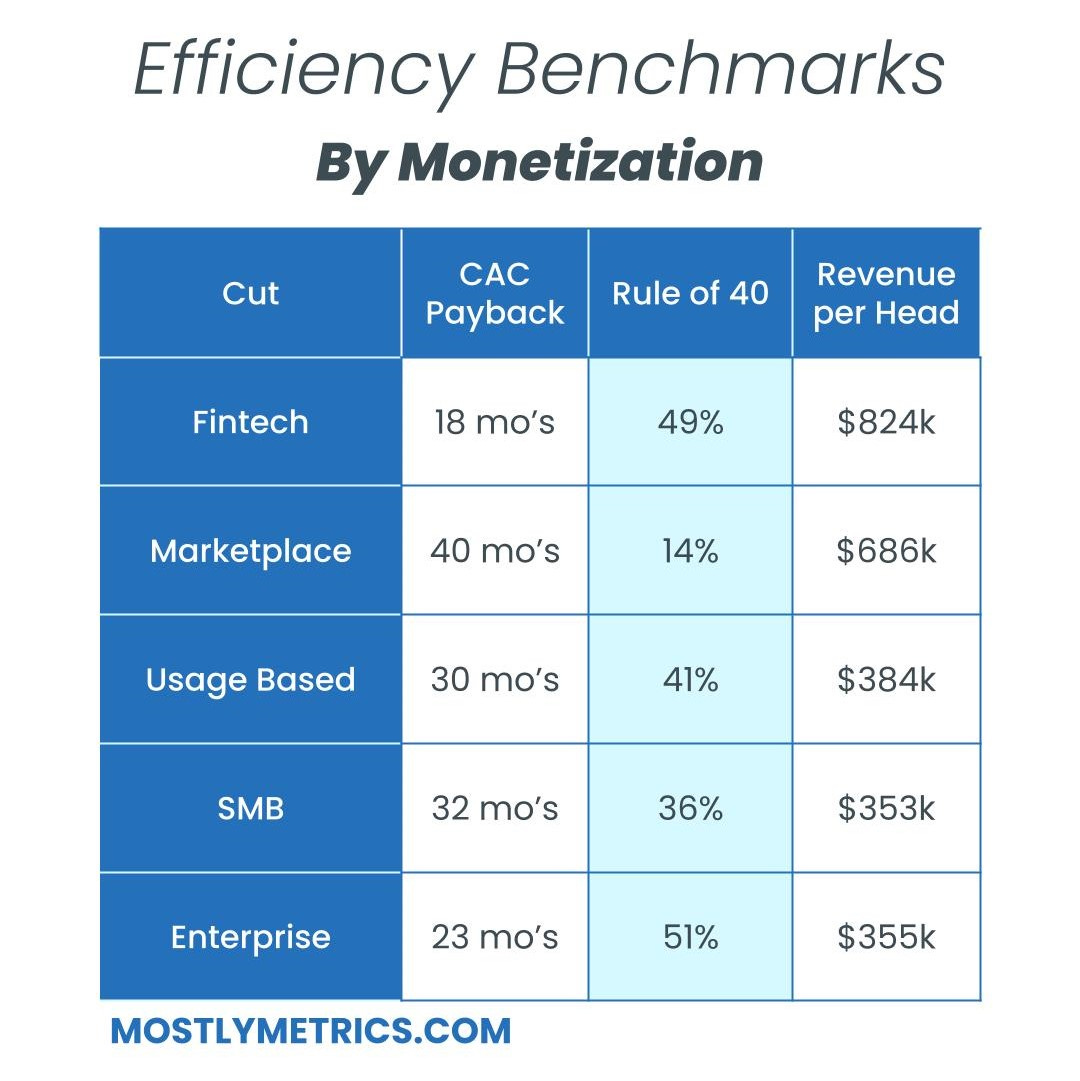

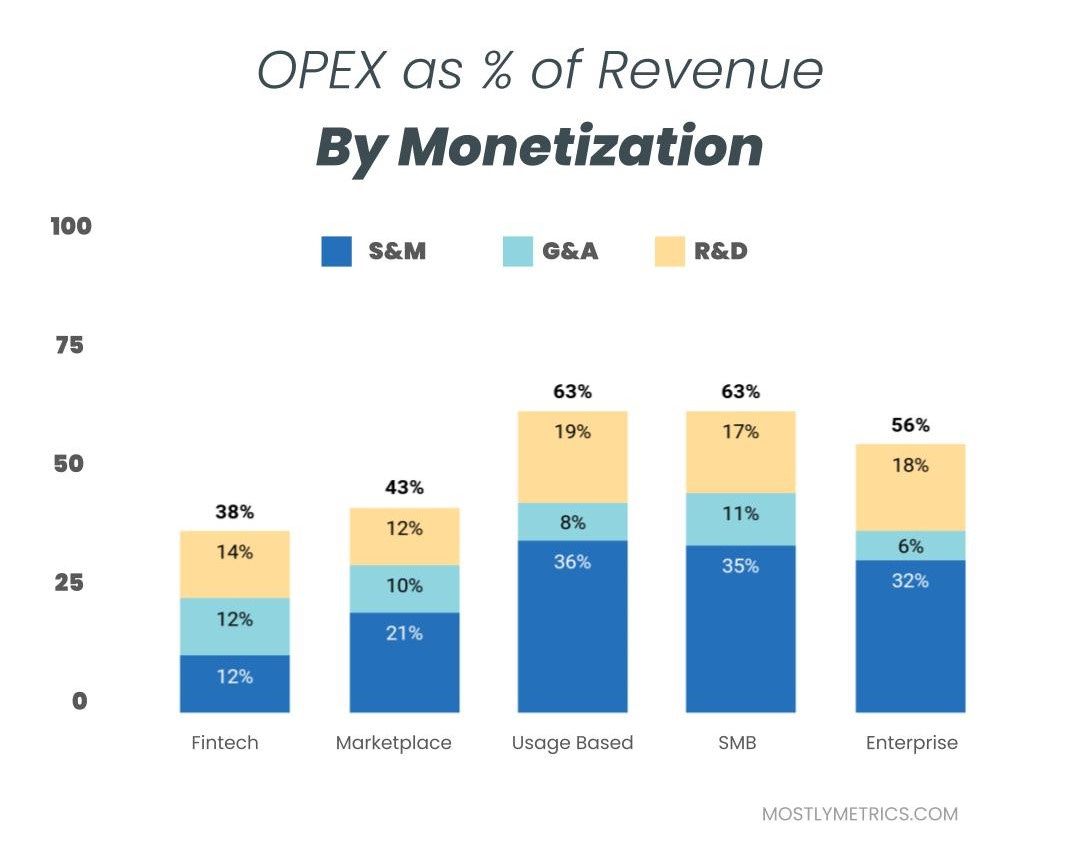

SMB is defined as average customer size below $100K in annual revenue

Enterprise is defined as average customer size above $100K in annual revenue

You can find the list of companies within each index here.

All definitions and formulas can be found here.

If you’d like the specific company level performance benchmarks used in these reports visit Virtua Research.

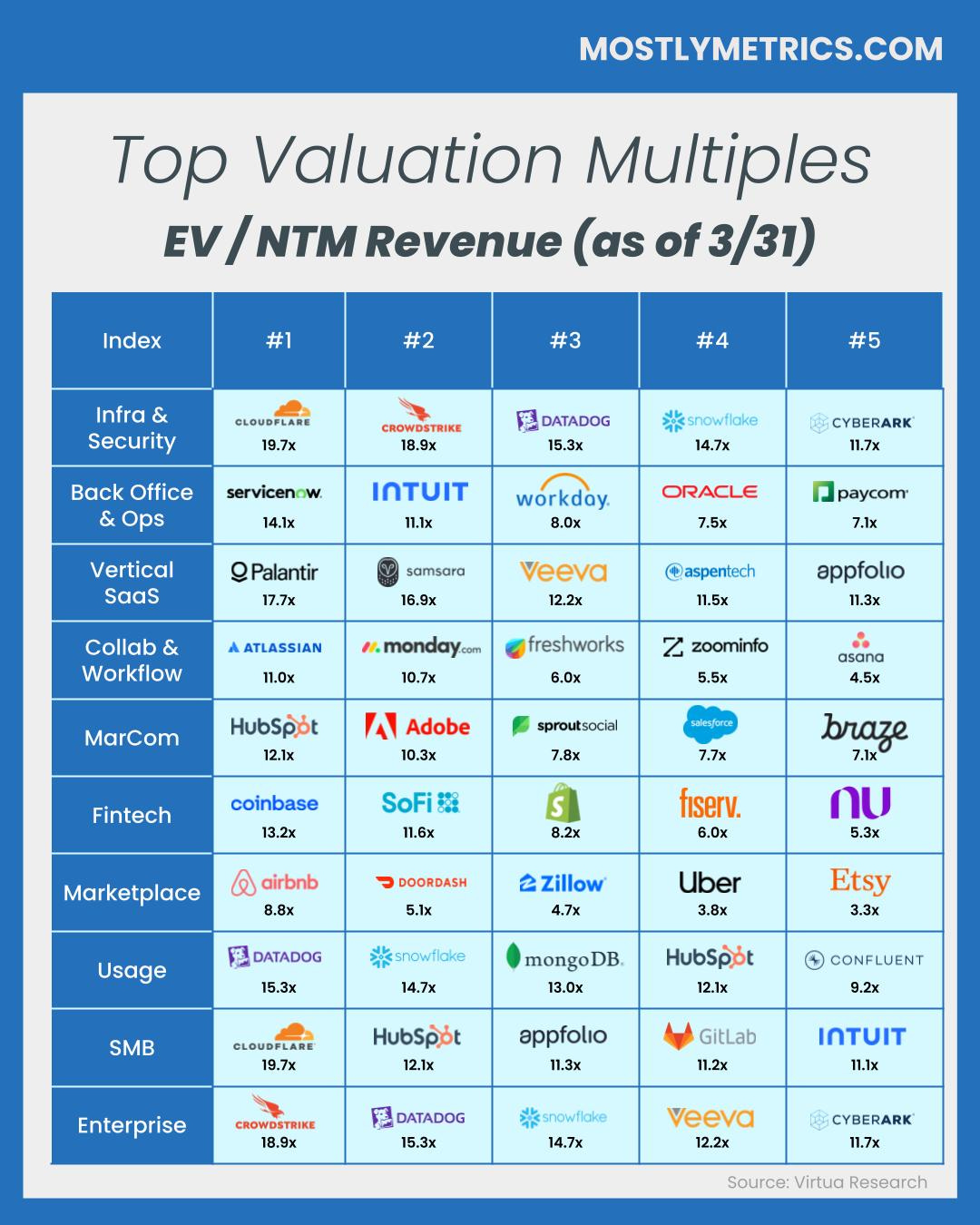

Revenue Multiples

Revenue multiples are a shortcut to compare valuations across the technology landscape, where companies may not yet be profitable. The most standard timeframe for revenue multiple comparison is on a “Next Twelve Months” (NTM Revenue) basis.

NTM is a generous cut, as it gives a company “credit” for a full “rolling” future year. It also puts all companies on equal footing, regardless of their fiscal year end and quarterly seasonality.

However, not all technology verticals or monetization strategies receive the same “credit” on their forward revenue, which operators should be aware of when they create comp sets for their own companies. That is why I break them out as separate “indexes”.

Reasons may include:

Recurring mix of revenue

Stickiness of revenue

Average contract size

Cost of revenue delivery

Criticality of solution

Total Addressable Market potential

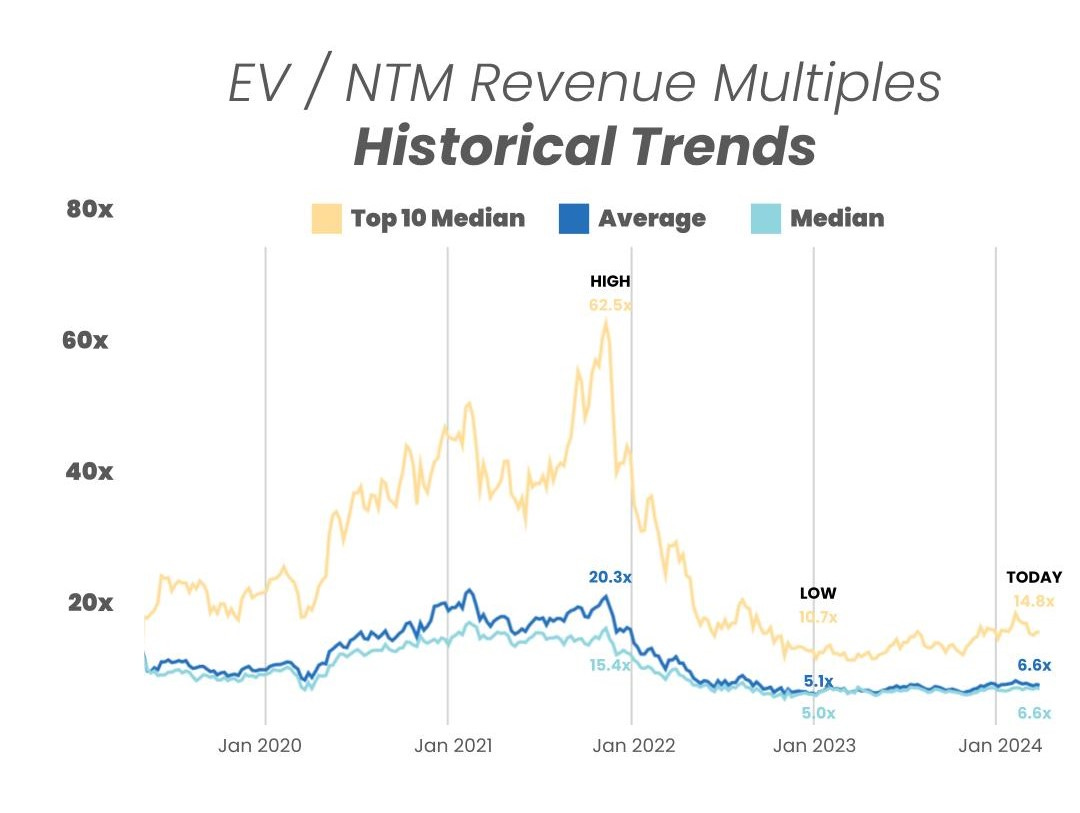

From a macro perspective, multiples trend higher in low interest environments, and vice versa.

Multiples shown are calculated by taking the Enterprise Value / NTM revenue.

Enterprise Value is calculated as: Market Capitalization + Total Debt - Cash

Market Cap fluctuates with share price day to day, while Total Debt and Cash are taken from the most recent quarterly financial statements available. That’s why we share this report each week - to keep up with changes in the stock market, and to update for quarterly earnings reports when they drop.

Historically, a 10x NTM Revenue multiple has been viewed as a “premium” valuation reserved for the best of the best companies.

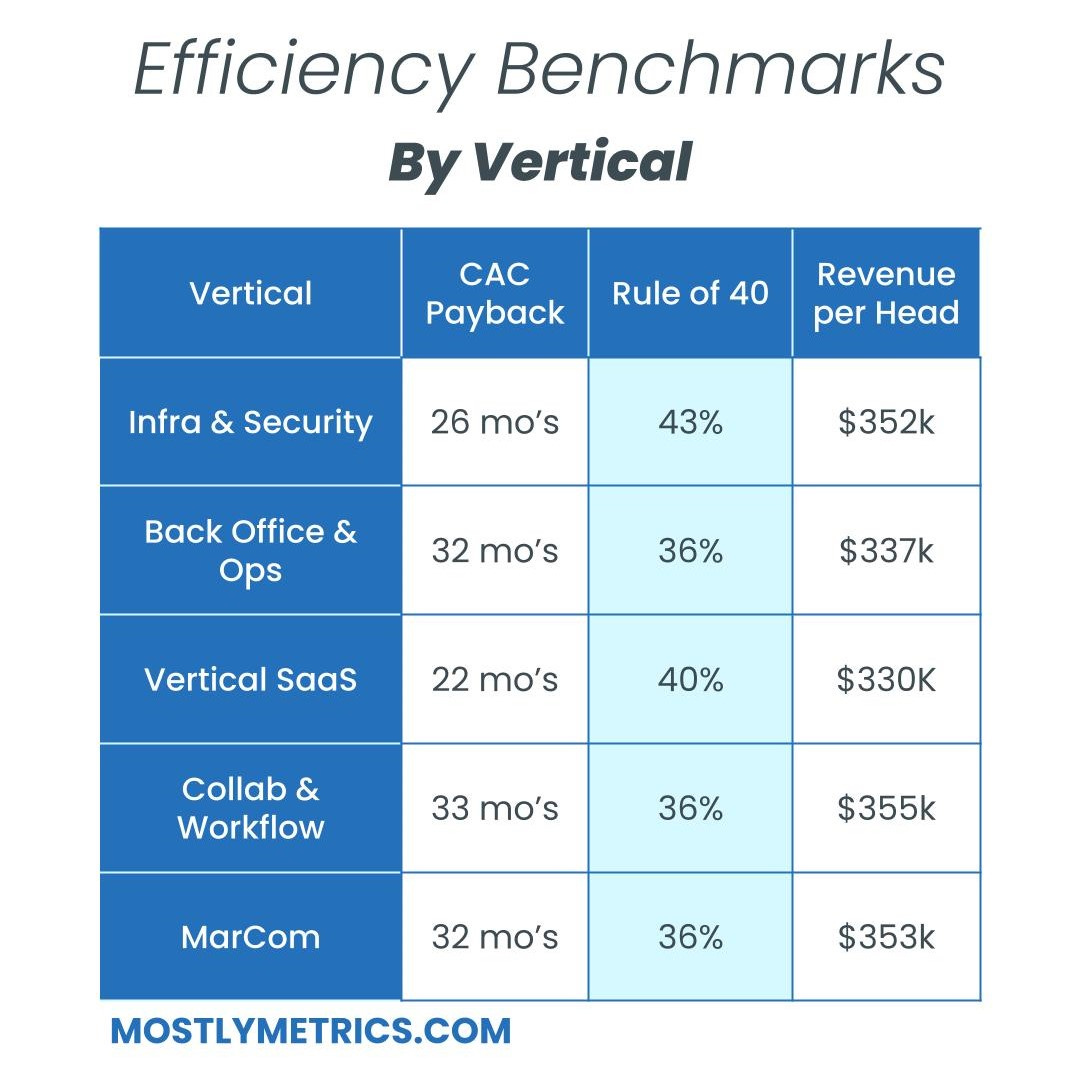

Efficiency Benchmarks

Companies who can do more with less tend to earn higher valuations.

Three of the most common, and consistently publicly available, metrics to measure efficiency include:

CAC Payback Period: How many months does it take to recoup the cost of acquiring a customer?

CAC Ratio is calculated as: (∆TTM Sales * Gross Profit Margin) / TTM S&M

CAC Payback Period is calculated as: (1 / CAC ratio) * 12

Note: Some may measure CAC Payback using the change in last quarter’s revenue x 4, but I believe this overstates a company’s progress if they are growing fast, and the output can be volatile due to quarterly sales seasonality. That’s why I look at it on a Trailing Twelve Month Basis.

Rule of 40: How does a company balance topline growth with bottom line efficiency? It’s the sum of the company’s revenue growth rate and free cash flow margin. Netting the two should get you above 40 to pass the test.

Rule of 40 is calculated as: Total Revenue Growth YoY % + Non Gaap Operating Profit Margin %

Non Gaap Free Cash Flow is calculated as: Net cash provided by operating activities, minus capital expenditures and minus capitalized software development costs.

Revenue per Employee: On a per head basis, how much in sales does the company generate each year? The rule of thumb is public companies should be doing north of $450k per employee at scale. This is simple division. And I believe it cuts through all the noise - there’s nowhere to hide.

Revenue per Employee is calculated as: (TTM Revenue / Total Current Employees)

A few other notes on efficiency metrics:

Net Dollar Retention is another great measure of efficiency, but many companies have stopped quoting it as an exact number, choosing instead to disclose if it’s above or below a threshold once a year. It’s also uncommon for marketplaces and fintechs to report it at all.

Most public companies don’t report net new ARR, and not all revenue is “recurring”, so I’m using annual change in TTM revenue timeframes as a proxy in my calculations. I admit this is a “stricter” view, as it is measuring change in net revenue, rather than gross revenue additions pre-churn.

A word from our sponsor Blue Rocket

A 1% change to your pricing plan can increase your bottom line by more than 10% 🤯.

The journey to price optimization is complex, but you don't have to navigate it alone.

BlueRocket's pricing experts have all operated companies before. And they’ve used that hands-on experience to help companies like Salesforce, Gitlab, Brex, Zendesk, and Google optimize their pricing.

Readers of this newsletter get a pricing audit with BlueRocket’s CEO Jason Kap.

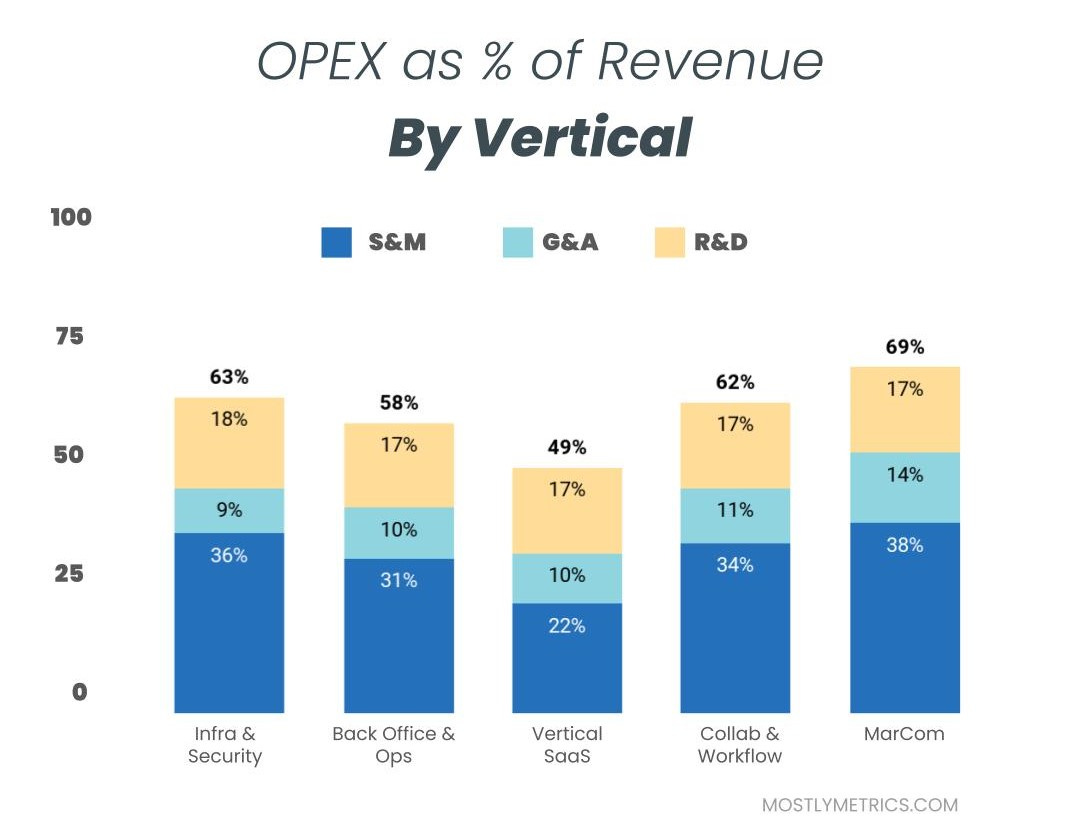

Operating Expenditures

Decreasing your OPEX relative to revenue demonstrates Operating Leverage, and leaves more dollars to drop to the bottom line, as companies strive to achieve +25% profitability at scale.

The three most common buckets companies put their operating costs into are:

Sales & Marketing: Sales and Marketing employees, advertising, demand gen, events, conferences, tools

Research & Development: Product and Engineering employees, development expenses, tools

General & Administrative: Finance, HR, and IT employees… and everything else. Or as I like to call myself “Strategic Backoffice Overhead”

All of these are taken on a non Gaap basis and therefore exclude stock based comp, a non cash expense. SBC is still an important figure to track for total comp and dilution purposes, though.

All benchmarking data provided by Virtua Research.

For assistance with your own benchmarking and equity research needs, contact cventi@virtuaresearch.com.

Tell him CJ sent you; he'll hook you up!"